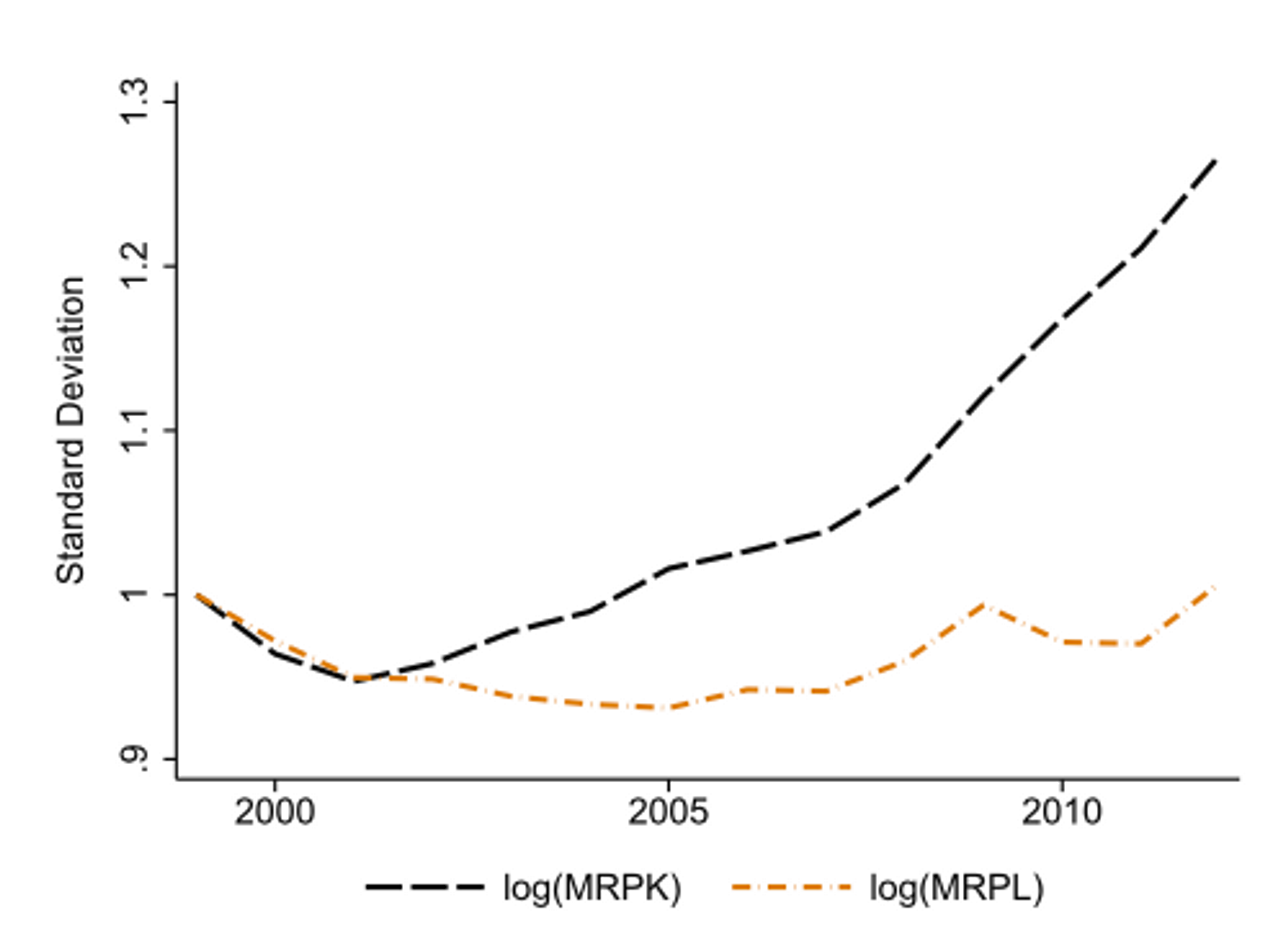

「究竟是什麼造成了經濟體之間成長的差異」,長久以來都是經濟學界的聖杯。本篇文章介紹研究「資源錯置 (Resource Misallocation)」的文獻,並說明資源錯置造成的問題,究竟如何與各國經濟發展的差異進行連結。

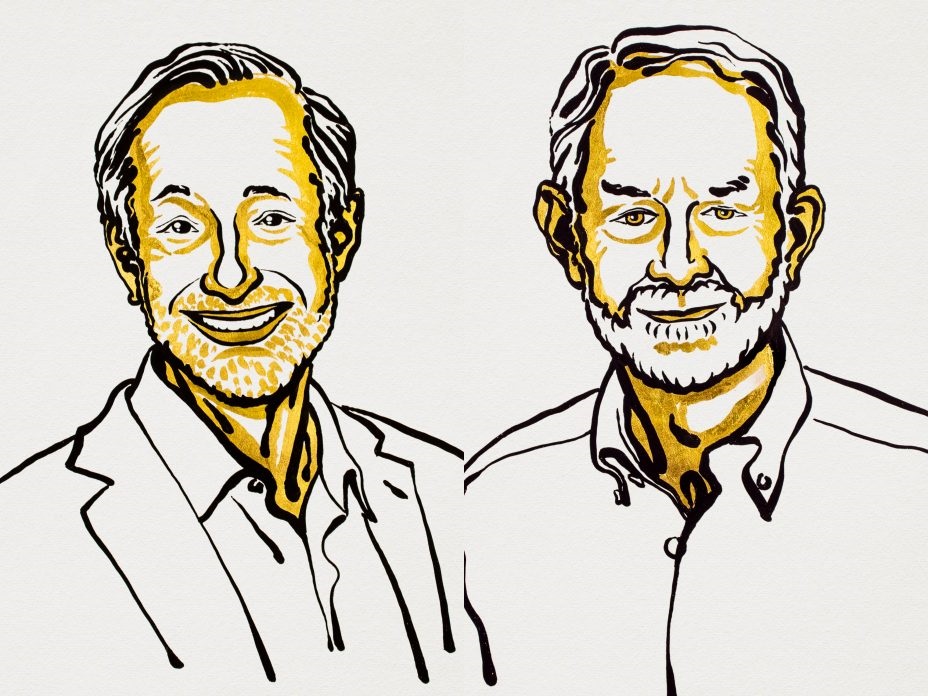

諾貝爾經濟學獎今年是頒給 Ben Bernanke, Douglas Diamond, Philip Dybvig 三位學者,表彰他們在銀行理論跟金融危機的研究。

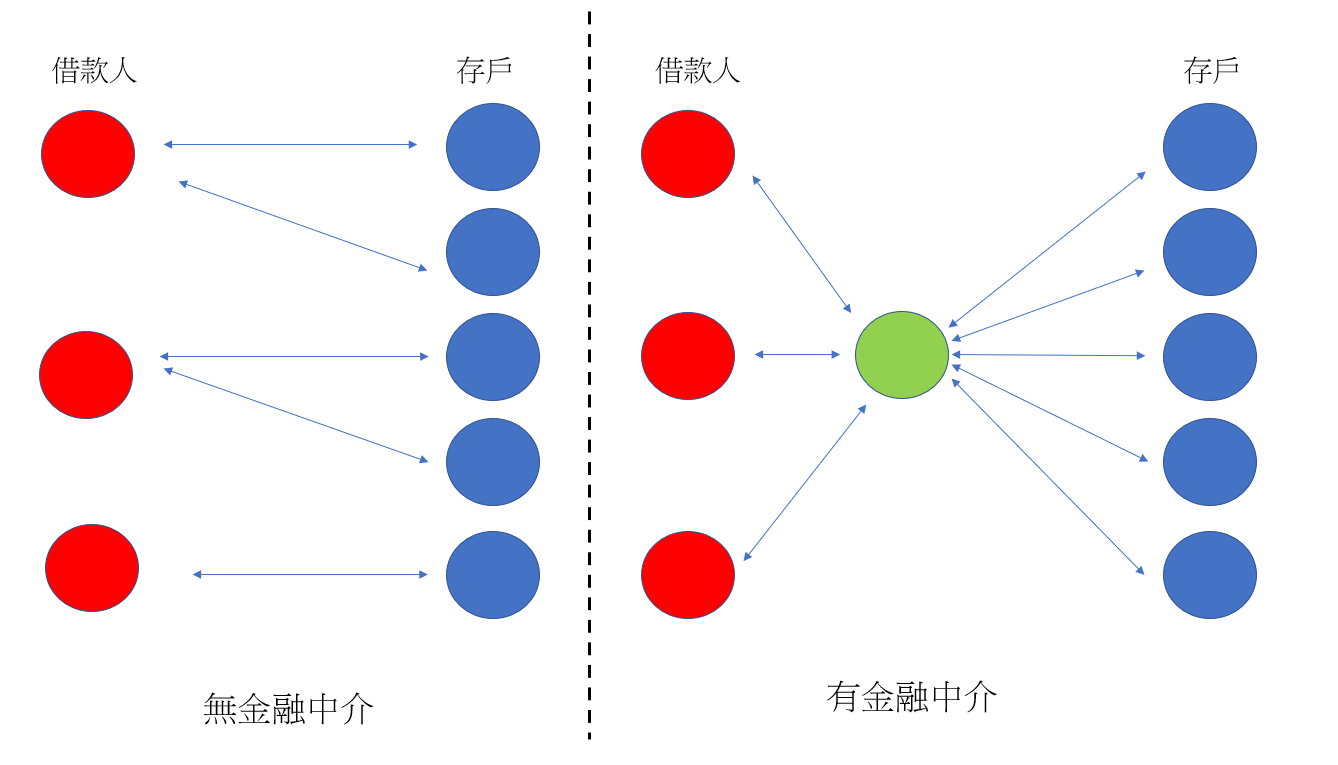

從 08 年金融海嘯起,《大賣空》、《華爾街之狼》、《半澤直樹》等作品多半都聚焦在失控的金融中介與其對應的黑暗面,這樣的觀點雖反映了部分問題,卻也不夠全面...

育嬰假對於夫妻雙方的效果是否相同?研究發現,在學術圈當中,在育嬰假期間「長聘鐘暫停」的政策事實上對男方更為有利,對女性的幫助相對卻較少。即使是限定女性的育嬰假,也並沒有對女性有更多幫助。這可能是家務分工不同造成的結果。

科學革命的動力是什麼?經濟學家的研究顯示:科學巨擘的凋亡,有時反而可以促進科學的進展。我們有沒有辦法從這個發現中,得到一些對於產業轉型的啟示呢?

2020年諾貝爾經濟學獎由保羅‧米爾格龍 (Paul Milgrom) 以及羅伯特‧威爾森 (Robert Wilson) 共同獲得,因為他們「對拍賣理論的改良以及新拍賣機制的研發」獲獎。威爾森和米爾格龍在前人對拍賣理論的基礎之上,進一步建立起了更一般化的架構。除此之外,他們還為政府的電磁波頻譜設計了拍賣制度。

星際大戰裡銀河共和國做星際交易時,長程貿易的投資報酬率怎麼訂的呢?如果哥倫布從來沒到達美洲而跌進了世界盡頭,美國還會不會和現在一樣蓬勃發展嗎?其實,這兩個都是曾經發表在經濟學期刊上的研究!今天帶大家了解一下,這兩篇莫名其妙的經濟學文章為什麼出現。如果能順便介紹一點經濟學那就更好了…

在這個大 Podcast 時代,來看看經濟系學生🦐挺的的 Econ Podcast 節目吧!

Bunching Method 是藉由使用行政資料來找尋因果關係,並將行政資料的聚集與經濟模型結合以萃取模型參數的計量方法。Bunching Method 不僅能用來找出有利政策執行的模型參數,也能用來識別一些外在因素干擾及不理性行為的效果及大小。

知識在經濟學的世界裡用途廣泛,我們這篇文章要討論的則是共有知識:你與我都知道某件事,而且你我都知道你我知道某件事,不止如此,你我甚至還知道你我知道你我知道某件事,而「知道」循環會無窮無盡的延伸下去。除了看了頭很痛外,你可能立即有了疑問,為什麼要那麼多層的「知道」?